版权说明:本文档由用户提供并上传,收益归属内容提供方,若内容存在侵权,请进行举报或认领

文档简介

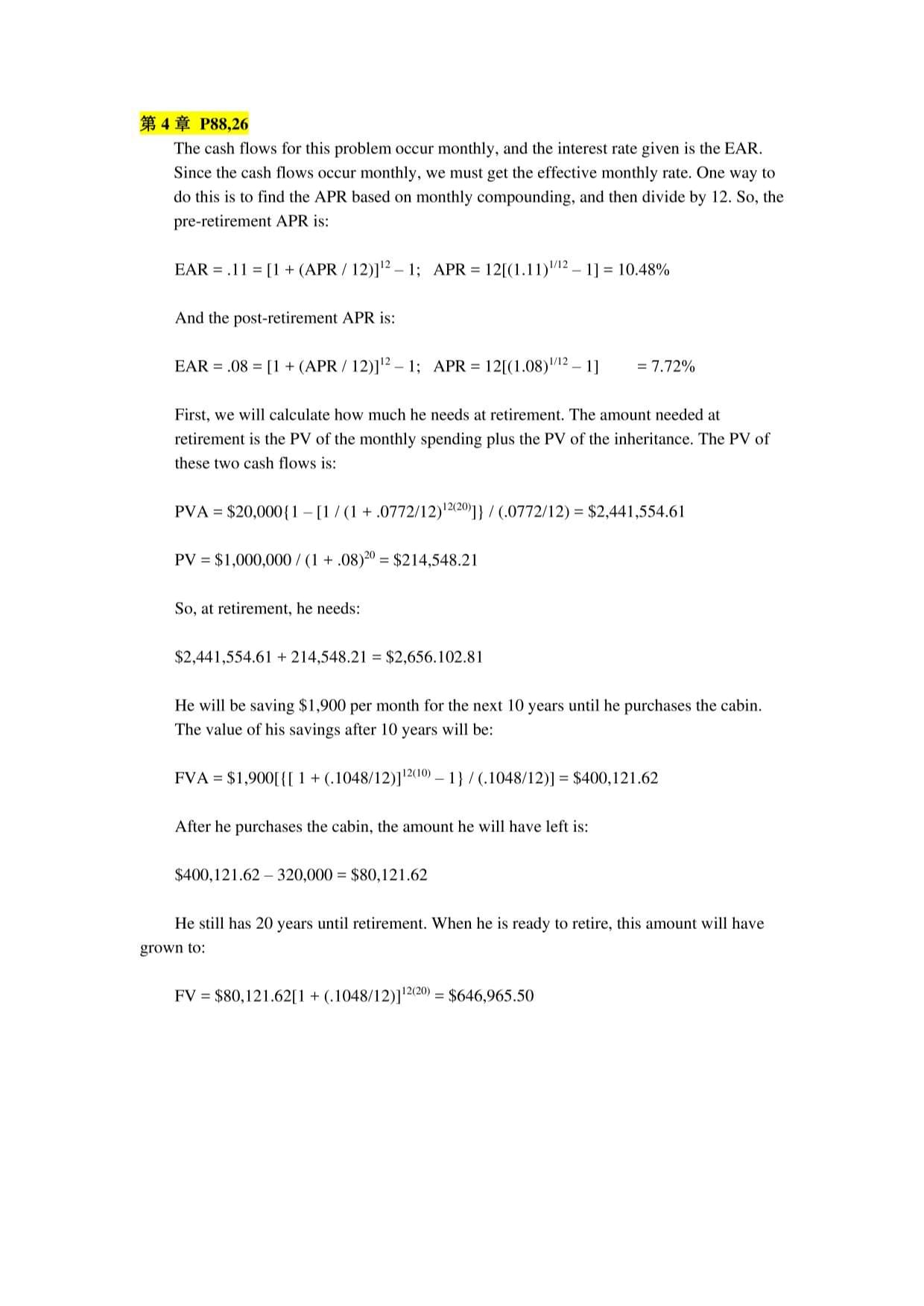

第4章第8,26

Thecashflowsforthisproblemoccurmonthly,andtheinterestrategivenistheEAR.

Sincethecashflowsoccurmonthly,wemustgettheeffectivemonthlyrate.Onewayto

dothisistofindtheAPRbasedonmonthlycompounding,andthendivideby12.So,the

pre-retirementAPRis:

EAR=.11=[1+(APR/12)]12-1;APR=12[(1.1l)l/12-1]=10.48%

Andthepost-retirementAPRis:

EAR=.08=[1+(APR/12)]12-1;APR=12[(1.08)l/12-1]=7.72%

First,wewillcalculatehowmuchheneedsatretirement.Theamountneededat

retirementisthePVofthemonthlyspendingplusthePVoftheinheritance.ThePVof

thesetwocashflowsis:

PVA=$20,000{l-[l/(l+.0772/12严°)]}/(.0772/12)=$2,441,554.61

PV=$1,000,000/(I+.08产=$214,548.21

So,atretirement,heneeds:

$2,441,554.61+214,548.21=$2,656.102.81

Hewillbesaving$1,900permonthforthenext10yearsuntilhepurchasesthecabin.

Thevalueofhissavingsafter10yearswillbe:

FVA=$l,900[{[1+(.1048/12)]12(10)-l}/(.1048/12)]=$400,121.62

Afterhepurchasesthecabin,theamounthewillhaveleftis:

$400,121.62-320,000=$80,121.62

Hestillhas20yearsuntilretirement.Whenheisreadytoretire,thisamountwillhave

grownto:

FV=$80,121.62[l+(.1048/12)]I2(20)=$646,965.50

So,whenheisreadytoretire,basedonhiscurrentsavings,hewillbeshort:

$2,656,102.81-645,965.50=$2,010,137.31

ThisamountistheFVofthemonthlysavingshemustmakebetweenyears10and30.

So,findingtheannuitypaymentusingtheFVAequation,wefindhismonthlysavings

willneedtobe:

FVA=$2,010,137.31=C[{[1+(.1048/12)]12(20)-1}/(.1048/12)]

C=$2,486.12

第5章Pl09,24

,a.TheprofitabilityindexisthePVofthefuturecashflowsdividedbytheinitial

investment.Theprofitabilityindexforeachprojectis:

2

PIA=[$140,000/1.12+$140,000/1.12]/$200,000=1.18

PIB=[$260,000/1.12+$260,000/1.122]/$400,000=1.10

PIc=[$150,000/1.12+$120,000/1.122]/$200,000=1.15

b.TheNPVofeachprojectis:

2

NPVA=-$200,000+$140,000/1.12+$140,000/1.12

NPVA=$36,607.14

2

NPVB=-$400,000+$260,000/1.12+$260,000/1.12

NPVB=$39,413.27

2

NPVC=-$200,000+$150,000/1.12+$120,000/1.12

NPVC=$29,591.84

c.AcceptprojectsA,B,andC.Sincetheprojectsareindependent,acceptallthree

projectsbecausetherespectiveprofitabilityindexofeachisgreaterthanone.

d.BNPV或增量PI

e.AB

第6章P128J3题

Wewillusethebottom-upapproachtocalculatetheoperatingcashflowforeachyear.

Wealsomustbesuretoincludethenetworkingcapitalcashflowseachyear.So,thenet

incomeandtotalcashfloweachyearwillbe:

Year1Year2Year3Year4

Sales$8,500$9,000$9,500$7,000

Costs1,9002,0002,2001,700

Depreciation4,0004,0004,0004,000

EBT$2,600$3,000$3,300$1,300

Tax8841,0201,122442

Netincome$1,716$1,980$2,178$858

OCF$5,716$5,980$6,178$4,858

Capitalspending-$16,000

NWC-200-250-300-200950

Incrementalcashflow-$16,200$5,466$5,680$5,978$5,808

TheNPVfortheprojectis:

NPV=-$16,200+$5,466/1.12+$5,680/1.122+$5,978/1.123+$5,808/1.124

NPV=$1,154.53

第7章P147J7题

WeneedtocalculatetheNPVofeachoption,andchoosetheoptionwiththehighest

NPV.So,theNPVofgoingdirectlytomarketis:

NPV=Csuccess(Prob,ofSuccess)

NPV=$1,500,000(0.50)

NPV=$750,000

TheNPVofthefocusgroupis:

NPV=Co+Csuccess(Prob,ofSuccess)

NPV=-$135,000+$1,500,000(0.65)

NPV=$840,000

AndtheNPVofusingtheconsultingfirmis:

NPV=Co+Csuccess(Prob,ofSuccess)

NPV=-$400,000+$1,500,000(0.85)

NPV=$875,000

ThefirmshouldusetheconsultingfirmsincethatoptionhasthehighestNPV.

第8章P171,25题

Thepriceofanybond(orfinancialinstrument)isthePVofthefuturecashflows.Even

thoughBondMmakesdifferentcouponspayments,tofindthepriceofthebond,wejust

findthePVofthecashflows.ThePVofthecashflowsforBondMis:

PM=$800(PVIFA4%j6)(PVIF4%j2)+$1,000(PVIFA4O^I2)(PVIF4%,28)+

$2O,OOO(PVIF4%,4O)

PM=$13,117.88

Noticethatforthecouponpaymentsof$800,wefoundthePVAforthecoupon

payments,andthendiscountedthelumpsumbacktotoday.

BondNisazerocouponbondwitha$20,000parvalue;therefore,thepriceofthebond

isthePVofthepar,or:

PN=$2O,OOO(PVIF4%,4O)=$4,165.78

第9章P191,7题

Hereweneedtofindthedividendnextyearforastockexperiencingdifferentialgrowth.

Weknowthestockprice,thedividendgrowthrates,andtherequiredreturn,butnotthe

dividend.First,weneedtorealizethatthedividendinYear3isthecurrentdividend

timestheFVIF.ThedividendinYear3willbe:

D3=Do(1.30)3

AndthedividendinYear4willbethedividendinYear3timesoneplusthegrowthrate,

or:

D4=Do(1.30)3(1.18)

Thestockbeginsconstantgrowthafterthe4thdividendispaid,sowecanfindtheprice

ofthestockinYear4asthedividendinYear5,dividedbytherequiredreturnminusthe

growthrate.TheequationforthepriceofthestockinYear4is:

P4=DMl+g)/(R—g)

NowwecansubstitutethepreviousdividendinYear4intothisequationasfollows:

P4=DO(1+(1+g2)(1+g3)/(R-g3)

3

P4=Do(1.30)(1.18)(1.08)/(.13-.08)=56.00D()

Whenwesolvethisequation,wefindthatthestockpriceinYear4is56.00timesas

largeasthedividendtoday.Nowweneedtofindtheequationforthestockpricetoday.

ThestockpricetodayisthePVofthedividendsinYears1,2,3,and4,plusthePVof

theYear4price.So:

223334

Po=Do(1.3O)/1.13+DO(1.3O)/1.13+Do(1.3O)/1.13+Do(1.3O)(1.18)/1.13+

56.OODo/1.134

WecanfactoroutD()intheequation,andcombinethelasttwoterms.Doingso,weget:

Po=$65.00=D(){1.30/1.13+1.302/l.132+1.303/l.133+[(1.3O)3(1.18)+56,00]/1.134)

Reducingtheequationevenfurtherbysolvingallofthetermsinthebraces,weget:

$65=$39.86D0

Do=$65.00/$39.86=$1.63

Thisisthedividendtoday,sotheprojecteddividendforthenextyearwillbe:

Di=$1.63(1.30)=$2.12

第10章P212,15-17

15.a.Tofindtheaveragereturn,wesumallthereturnsanddividebythenumberof

returns,so:

Arithmeticaveragereturn=(.34+.16+.19-.21+.08)/5

Arithmeticaveragereturn=.1120or11.20%

b.Usingtheequationtocalculatevariance,wefind:

Variance=l/4[(.34-.112)2+(.16-.H2)2+(.19-.112)2+(-.21-.112,+

(.08-.112)2]

Variance=0.041270

So,thestandarddeviationis:

Standarddeviation=(0.041270)12

Standarddeviation=0.2032or20.32%

16.a.Tocalculatetheaveragerealreturn,wecanusetheaveragereturnoftheassetand

theaverageinflationrateintheFisherequation.Doingso,wefind:

(1+R)=(1+r)(l+h)

r=(1.1120/1.042)-1

r=.0672or6.72%

b.Theaverageriskpremiumissimplytheaveragereturnoftheasset,minusthe

averagerealrisk-freerate,so,theaverageriskpremiumfbrthisassetwouldbe:

RP=R-Rf

RP=.1120-,0510

RP=.0610or6.10%

17.Wecanfindtheaveragerealrisk-freerateusingtheFisherequation.Theaveragereal

risk-freeratewas:

(1+R)=(1+r)(l+h)

rf=(1.051/1.042)-1

rf=.0086or0.86%

Andtocalculatetheaveragerealriskpremium,wecansubtracttheaveragerisk-freerate

fromtheaveragerealreturn.So,theaveragerealriskpremiumwas:

rp=r-rf=6.72%-0.86%

rp=5.85%

18.Applythefive-yearholding-periodreturnformulatocalculatethetotalreturnofthe

stockoverthefive-yearperiod,wefind:

5-yearholding-periodreturn=[(1+Ri)(l+R2)(l+R3XI+&)(1+R5)]-1

5-yearholding-periodreturn=[(1+.1843)(1+.1682)(1+.0683)(1+.3219)(1-.1987)]

-1

5-yearholding-periodreturn=0.5655or56.55%

22.Tocalculatethearithmeticandgeometricaveragereturns,wemustfirstcalculatethe

returnforeachyear.Thereturnforeachyearis:

Ri=($55.83-49.62+0.68)/$49.62=.1389or13.89%

R2=($57.03-55.83+0.73)/$55.83=.0346or3.46%

R3=($50.25-57.03+0.84)/$57.03=-.1042or-10.42%

R4=($53.82-50.25+0.91)/$50.25=.0892or8.92%

R5=($64.18-53.82+1.02)/$53.82=.2114or21.14%

Thearithmeticaveragereturnwas:

RA=(0.1389+0.0346-0.1042+0.0892+0.2114)/5

RA=0.0740or7.40%

Andthegeometricaveragereturnwas:

RG=[(1+.1389)(1+.0346)(1-.1042)(1+.0892)(1+.2114)]1/5-1

RG=0.0685or6.85%

第11章P240:27

a.Again,wehaveaspecialcasewheretheportfolioisequallyweighted,sowecan

sumthereturnsofeachassetanddividebythenumberofassets.Theexpected

returnoftheportfoliois:

E(RP)=(.103+.05)/2=.0765or7.65%

b.Weneedtofindtheportfolioweightsthatresultinaportfoliowithapof0.50.We

knowthepoftherisk-freeassetiszero.Wealsoknowtheweightoftherisk-free

assetisoneminustheweightofthestocksincetheportfolioweightsmustsumto

one,or100percent.So:

pp=0.50=ws(.92)+(l-ws)(0)

0.50=,92ws+0-Ows

ws=0.50/.92

ws=.5435

And,theweightoftherisk-freeassetis:

WRf=l—.5435=4565

c.Weneedtofindtheportfolioweightsthatresultinaportfoliowithanexpected

returnof9percent.Wealsoknowtheweightoftherisk-freeassetisoneminusthe

weightofthestocksincetheportfolioweightsmustsumtoone,or100percent.So:

E(RP)=.09=.103ws+.05(1-ws)

.09=.103ws+.05-.05ws

ws=.7547

So,thepoftheportfoliowillbe:

PP=.7547(.92)+(1-.7547)(0)=0.694

d.Solvingforthepoftheportfolioaswedidinparta,wefind:

P

P=1.84=ws(.92)+(1-ws)(0)

ws=1.84/.92=2

WRf=1-2=-l

Theportfolioisinvested200%inthestockand-100%intherisk-freeasset.This

representsborrowingattherisk-freeratetobuymoreofthestock.

第12章P256:12

a.Ifmisthesystematicriskportionofreturn,then:

GNP

m-PAGNP+PinnationAInflation+prAInterestrates

/n=.0000479($13,601-13,275)-1.30(3.20%-3.90%)-.67(4.70%-5.20%)

a=2.81%

b.Theunsystematicreturnisthereturnthatoccursbecauseofafirmspecificfactor

suchasthebadnewsaboutthecompany.So,theunsystematicreturnofthestockis

-2.6percent.Thetotalreturnistheexpectedreturn,plusthetwocomponentsof

unexpectedreturn:thesystematicriskportionofreturnandtheunsystematic

portion.So,thetotalreturnofthestockis:

R=R+/n+8

R=10.80%+2.81%-2.6%

R=11.01%

P257:16

a.Themarketmodelisspecifiedby:

R=R+B(RM-RM)+e

soapplyingthattoeachStock:

StockA:

RA=RA+PA(RM—RM)+'A

A

R=10.5%+1.2(RM-14.2%)+£A

StockB:

RB=RB+BB(RM-RM)+£B

B

R=13.0%+0.98(RM-14.2%)+8B

StockC:

Rc=Rc+PC(RM-RM)+£C

Rc=15.7%+1.37(RM-14.2%)+£C

b.Sincewedon'thavetheactualmarketreturnorunsystematicrisk,wewillgeta

formulawiththosevaluesasunknowns:

Rp—.3ORA+.45RB+.25Rc

RP=.30(10.5%+1.2(RM-14.2%)+£A]+.45[13.0%+0.98(RM-14.2%)+8B]

+.25[15.7%+1.37(RM-14.2%)+8C]

RP=.30(10.5%)+.45(13%)+.25(15.7%)+[.30(1.2)+.45(.98)+.25(1.37)](RM-

14.2%)

+.308A+.45£B+.258c

RP=12.925%+1.1435(RM-14.2%)+.30sA+453+.25EC

c.Usingthemarketmodel,ifthereturnonthemarketis15percentandthesystematic

riskiszero,thereturnforeachindividualstockis:

RA=10.5%+1.20(15%-14.2%)

RA=11.46%

RB=13%+0.98(15%-14.2%)

RB=13.78%

Rc=15.70%+1.37(15%-14.2%)

Rc=16.80%

Tocalculatethereturnontheportfolio,wecanusetheequationfrompartb,so:

RP=12.925%+1.1435(15%-14.2%)

RP=13.84%

Alternatively,tofindtheportfolioreturn,wecanusethereturnofeachassetandits

portfolioweight,o亡

Rp—XjRi+X2R2+X3R3

RP=.30(11.46%)+.45(13.78%)+.25(16.80%)

RP=13.84%

第13章

P280:11,12,13,14,18,19

11.Withtheinformationgiven,wecanfindthecostofequityusingthedividendgrowth

model.Usingthismodel,thecostofequityis:

RE=[$2.40(1.055)/$52]+.055=.1037or10.37%

12.WehavetheinformationavailabletocalculatethecostofequityusingtheCAPMand

thedividendgrowthmodel.UsingtheCAPM,wefind:

RE=.05+0.85(.08)=.118()or11.80%

Andusingthedividendgrowthmodel,thecostofequityis

RE=[$1.60(1.06)/$37]+.06=.1058or10.58%

Bothestimatesofthecostofequityseemreasonable.Ifwerememberthehistorical

returnonlargecapitalizationstocks,theestimatefromtheCAPMmodelisaboutthe

sameasthehistoricalaverage,andtheestimatefromthedividendgrowthmodelisabout

onepercentlowerthanthehistoricalaverage,sowecannotdefinitivelysayoneofthe

estimatesisincorrect.Giventhis,wewouldusetheaverageofthetwo,so:

RE=(.1180+.1058)/2=.1119or11.19%

13.a.ThepretaxcostofdebtistheYTMofthecompany'sbonds,so:

Po=$1,080=$35(PVIFAR%,46)+$l,000(PVIFR%,46)

R=3.167%

YTM=2x3.167%=6.33%

b.Theaftertaxcostofdebtis:

RD=.0633(1-.35)=.0412or4.12%

c.Theaftertaxrateismorerelevantbecausethatistheactualcosttothecompany.

14.UsingtheequationtocalculatetheWACC,wefind:

WACC=.70(.15)+.30(.08)(l-.35)=.1206or12.06%

18.a.Heshouldlookattheweightedaverageflotationcost,notjustthedebtcost.

b.Theweightedaverageflotationcostistheweightedaverageoftheflotationcosts

fordebtandequity,so:

fT=.05(.75/1.75)+.08(1/1.75)=.0671or6.71%

c.Thetotalcostoftheequipmentincludingflotationcostsis:

Amountraised(1-.0671)=$20,000,000

Amountraised=$20,000,000/(1-.0671)=$21,439,510

Evenifthespecificfundsareactuallybeingraisedcompletelyfromdebt,the

flotationcosts,andhencetrueinvestmentcost,shouldbevaluedasifthefirm's

targetcapitalstructureisused.

19.Usingthedebt-equityratiotocalculatetheWACC,wefind:

WACC=(.65/1.65)(.055)+(1/1.65)(.15)=.1126or11.26%

Sincetheprojectisriskierthanthecompany,weneedtoadjusttheprojectdiscountrate

fortheadditionalrisk.Usingthesubjectiveriskfactorgiven,wefind:

Projectdiscountrate=11.26%+2.00%=13.26%

WewouldaccepttheprojectiftheNPVispositive.TheNPVisthePVofthecash

outflowsplusthePVofthecashinflows.Sincewehavethecosts,wejustneedtofind

thePVofinflows.Thecashinflowsareagrowingperpetuity.Ifyouremember,the

equationforthePVofagrowingperpetuityisthesameasthedividendgrowthequation,

so:

PVoffutureCF=$3,500,000/(.1326-,05)=$42,385,321

Theprojectshouldonlybeundertakenifitscostislessthan$42,385,321sincecostsless

thanthisamountwillresultinapositiveNPV.

第15章

P322:2,4,6,12,15,16,21

2.Thedifferencesbetweenpreferredstockanddebtare:

a.Thedividendsonpreferredstockcannotbedeductedasinterestexpensewhen

determiningtaxablecorporateincome.Fromtheindividualinvestor'spointofview,

preferreddividendsareordinaryincomefbrtaxpurposes.Forcorporateinvestors,

70%oftheamounttheyreceiveasdividendsfrompreferredstockareexemptfrom

incometaxes.

h.Incaseofliquidation(atbankruptcy),preferredstockisjuniortodebtandseniorto

commonstock.

c.Thereisnolegalobligationforfirmstopayoutpreferreddividendsasopposedto

theobligatedpaymentofinterestonbonds.Therefore,firmscannotbeforcedinto

defaultifapreferredstockdividendisnotpaidinagivenyear.Prefeneddividends

canbecumulativeornon-cumulative,andtheycanalsobedeferredindefinitely(of

course,indefinitelydeferringthedividendsmighthaveanundesirableeffectonthe

marketvalueofthestock).

4.Thereturnonnon-convertiblepreferredstockislowerthanthereturnoncorporate

bondsfortworeasons:1)Corporateinvestorsreceive70percenttaxdeductibilityon

dividendsiftheyholdthestock.Therefore,theyarewillingtopaymoreforthestock;

thatlowersitsreturn.2)Issuingcorporationsarewillingandabletoofferhigherreturns

ondebtsincetheinterestonthedebtreducestheirtaxliabilities.Preferreddividendsare

paidoutofnetincome,hencetheyprovidenotaxshield.

Corporateinvestorsaretheprimaryholdersofpreferredstocksince,unlikeindividual

investors,theycandeduct70percentofthedividendwhencomputingtheirtaxliabilities.

Therefore,theyarewillingtoacceptthelowerreturnthatthestockgenerates.

6.Therearetwobenefits.First,thecompanycantakeadvantageofinterestratedeclinesby

callinginanissueandreplacingitwithalowercouponissue.Second,acompanymight

wishtoeliminateacovenantforsomereason.Callingtheissuedoesthis.Thecosttothe

companyisahighercoupon.Aputprovisionisdesirablefromaninvestor'sstandpoint,

soithelpsthecompanybyreducingthecouponrateonthebond.Thecosttothe

companyisthatitmayhavetobuybackthebondatanunattractiveprice.

12.Whenacompanyhasdualclassstock,thedifferenceintheshareclassesarethevoting

rights.Dualshareclassesallowminorityshareholderstoretaincontrolofthecompany

eventhoughtheydonotownamajorityofthetotalsharesoutstanding.Often,dualshare

companieswerestartedbyafamily,takenpublic,butthefounderswanttoretaincontrol

ofthecompany.

16.Ifthecompanyusesstraightvoting,theboardofdirectorsiselectedoneatatime.You

willneedtoownone-halfoftheshares,plusoneshare,inordertoguaranteeenough

votestowintheelection.So,thenumberofsharesneededtoguaranteeelectionunder

straightvotingwillbe:

Sharesneeded=(600,000shares/2)+1

Sharesneeded=300,001

Andthetotalcosttoyouwillbethesharesneededtimesthepricepershare,or:

Totalcost=300,001x$39

Totalcost=$11,700,039

Ifthecompanyusescumulativevoting,theboardofdirectorsareallelectedatonce.You

willneed1/(N+1)percentofthestock(plusoneshare)toguaranteeelection,whereNis

thenumberofseatsupforelection.So,thepercentageofthecompany'sstockyouneed

is:

Percentofstockneeded=1/(N+1)

Percentofstockneeded=1/(7+1)

Percentofstockneeded=.1250or12.50%

So,thenumberofsharesyouneedtopurchaseis:

Numberofsharestopurchase=(600,000x.1250)+1

Numberofsharestopurchase=75,001

Andthetotalcosttoyouwillbethesharesneededtimesthepricepershare,or:

Totalcost=75,001x$39

Totalcost=$2,925,039

第16章P342:11、12、13、14、15

11-13seeexcel

14.a.UnderPlanI,theunleveredcompany,netincomeisthesameasEBITwithno

corporatetax.TheEPSunderthiscapitalizationwillbe:

EPS=$750,000/240,000shares

EPS=$3.13

UnderPlanII,theleveredcompany,EBITwillbereducedbytheinterestpayment.

Theinterestpaymentistheamountofdebttimestheinterestrate,so:

NI=$750,000-.10($3,100,000)

NI=$440,000

AndtheEPSwillbe:

EPS=$440,000/160,000shares

EPS=$2.75

PlanIhasthehigherEPSwhenEBITis$750,000.

h.UnderPlanI,thenetincomeis$1,500,000andtheEPSis:

EPS=$1,500,000/240,000shares

EPS=$6.25

UnderPlanII,thenetincomeis:

NI=$1,500,000-.10($3,l00,000)

NI=$1,190,000

AndtheEPSis:

EPS=$1,190,000/160,000shares

EPS=$7.44

PlanIIhasthehigherEPSwhenEBITis$1,500,000.

c.TofindthebreakevenEBITfortwodifferentcapitalstructures,wesimplysetthe

equationsforEPSequaltoeachotherandsolveforEBIT.ThebreakevenEBITis:

EBIT/240,000=[EBIT-.10($3,100,000)]/160,000

EBIT=$930,000

15.Wecanfindthepricepersharebydividingtheamountofdebtusedtorepurchaseshares

bythenumberofsharesrepurchased.Doingso,wefindthesharepriceis:

Samevalue:240000*Shareprice=160000*Shareprice+3100000

Shareprice=$3,100,000/(240,000-160,000)

Shareprice=$38.75pershare

Thevalueofthecompanyundertheall-equityplanis:

V=$38.75(240,000shares)=$9,300,000

Andthevalueofthecompanyundertheleveredplanis:

V=$38.75(160,000shares)+$3,100,000debt=$9,300,000

第17章P368:18

18.a.Ifthecompanydecidestoretireallofitsdebt,itwillbecomeanunleveredfirm.

Thevalueofanall-equityfirmisthepresentvalueoftheaftertaxcashflowto

equityholders,whichwillbe:

Vu=(EBIT)(l-fc)//?o

Vu=($1,300,000)(1-.35)/.20

Vu=$4,225,000

b.Sincetherearenobankruptcycosts,thevalueofthecompanyasaleveredfirmis:

VL=Vu+{1-[(1-fc)/(1-)])xB

VL=$4,225,000+{1-[(1-.35)/(1-.25)]}x$2,500,000

=$4,558,333.33

c.Thebankruptcycostswouldnotaffectthevalueoftheunleveredfirmsinceitcould

neverbeforcedintobankruptcy.So,thevalueoftheleveredfirmwithbankruptcy

wouldbe:

VL=Vu+{1-[(1-rc)/(l-rB)]}xfi-C(B)

VL=($4,225,000+{1-((1-.35)/(I-.25)]}x$2,500,000)-$400,000

VL=$4,158,333.33

Thecompanyshouldchoosetheall-equityplanwiththisbankruptcycost.

第18章P382:15

15.a.Ifthecompanywerefinancedentirelybyequity,thevalueofthefirmwouldbe

equaltothepresentvalueofitsunleveredafter-taxearnings,discountedatits

unleveredcostofcapital.First,weneedtofindthecompany'sunleveredcashflows,

whichare:

Sales$28,900,000

Variablecosts17,340,000

EBT$11,560,000

Tax4,624,000

Netincome$6,936,000

So,thevalueoftheunleveredcompanyis:

Vu=$6,936,000/.17

Vu=$40,800,000

h.AccordingtoModigliani-MillerPropositionIIwithcorporatetaxes,thevalueof

leveredequityis:

Rs=Ro+(B/S)(R()-RB)(1—tc)

Rs=.17+(,35)(.17-.09)(1-.40)

Rs=.1868or18.68%

Inaworldwithcorporatetaxes,afirm'sweightedaveragecostofcapitalequals:

RWACC=[B/(B+S)](l-tc)RB+[S/(B+S)]Rs

Soweneedthedebt-valueandequity-valueratiosforthecompany.Thedebt-equity

ratioforthecompanyis:

B/S=0.35

B=0.35S

Substitutingthisinthedebt-valueratio,weget:

B/V=.35S/(.35S+S)

B/V=.35/1.35

B/V=.26

Andtheequity-valueratioisoneminusthedebt-valueratio,or:

S/V=1-.26

S/V=.74

So,usingthecapitalstructureweights,thecompany'sWACCis:

RWACC=[B/(B+S)](l-tc)RB+[S/(B+S)]Rs

RWACC=.26(1-.40)(.09)+.74(.1868)

RWACC=.1524or15.24%

Wecanusetheweightedaveragecostofcapitaltodiscountthefirm'sunlevered

aftertaxearningstovaluethecompany.Doingso,wefind:

VL=$6,936,000/.1524

VL=$45,520,661.16

Nowwecanusethedebt-valueratioandequity-valueratiotofindthevalueofdebt

andequity,whichare:

B=Vt(Debt-value)

B=$45,520,661.16(.26)

B=$11,801,652.89

S=Vb(Equity-value)

S=$45,520,661.16(.74)

S=$33,719,008.26

d.Inordertovalueafirm'sequityusingtheflow-to-equityapproach,wecandiscount

thecashflow

温馨提示

- 1. 本站所有资源如无特殊说明,都需要本地电脑安装OFFICE2007和PDF阅读器。图纸软件为CAD,CAXA,PROE,UG,SolidWorks等.压缩文件请下载最新的WinRAR软件解压。

- 2. 本站的文档不包含任何第三方提供的附件图纸等,如果需要附件,请联系上传者。文件的所有权益归上传用户所有。

- 3. 本站RAR压缩包中若带图纸,网页内容里面会有图纸预览,若没有图纸预览就没有图纸。

- 4. 未经权益所有人同意不得将文件中的内容挪作商业或盈利用途。

- 5. 人人文库网仅提供信息存储空间,仅对用户上传内容的表现方式做保护处理,对用户上传分享的文档内容本身不做任何修改或编辑,并不能对任何下载内容负责。

- 6. 下载文件中如有侵权或不适当内容,请与我们联系,我们立即纠正。

- 7. 本站不保证下载资源的准确性、安全性和完整性, 同时也不承担用户因使用这些下载资源对自己和他人造成任何形式的伤害或损失。

最新文档

- 跨平台架构设计的原则试题及答案

- 酒店菜单设计与管理试题及答案

- 2024年网络工程师职业挑战试题及答案

- 冷库电气安装工程施工方案

- 2025年油料生产项目合作计划书

- 智能合约漏洞检测报告

- 2025年紫外光固化油墨合作协议书

- 大概念视角下高中地理单元教学设计研究

- 2025年油基型密封胶项目建议书

- 基于特征融合的函数型数据分类研究

- 《汽车道路照明装置及系统》(征求意见稿)

- 残疾人法律援助知识讲座

- 小红书食用农产品承诺书示例

- 父亲角色对幼儿社会性发展的影响的研究

- 农业技术员培训培训课件

- AVL-CRUISE-2019-整车经济性动力性分析操作指导书

- 锂电池 应急预案

- 华为供应链管理(6版)

- 全国小学英语赛课一等奖绘本课《Big Cat Babies》

- 幕墙层间防火封堵施工技术交底

- 地球科学课件:冰川及冰川作用

评论

0/150

提交评论