付费下载

下载本文档

版权说明:本文档由用户提供并上传,收益归属内容提供方,若内容存在侵权,请进行举报或认领

文档简介

1、1MN50325Financial Accounting 2 Lecture 5David BenceLearning ObjectivesExamine Fair values, contingent consideration, purchased goodwillUnderstand Consolidated e Statements, including cancelling intra-group transactionsPurchased Goodwill CalculationMeasure the cost of the business combination (exclud

2、e acquisition-related costs which are expensed)Measure the separable assets, liabilities and any contingent liabilities controlled at fair valueDifference is purchased goodwill a non-current asset shown on consolidated SoFPFor example, pay 1m for net assets of 600,000 then purchased goodwill would b

3、e 400,000IFRS3 Rules on Consideration PaidThe fair value of consideration needs to be identifiedThis may be cash, shares or cash and sharesSome of the consideration may be deferred and/or be dependent on future profits. If deferred consideration is likely to be paid then the present value of the def

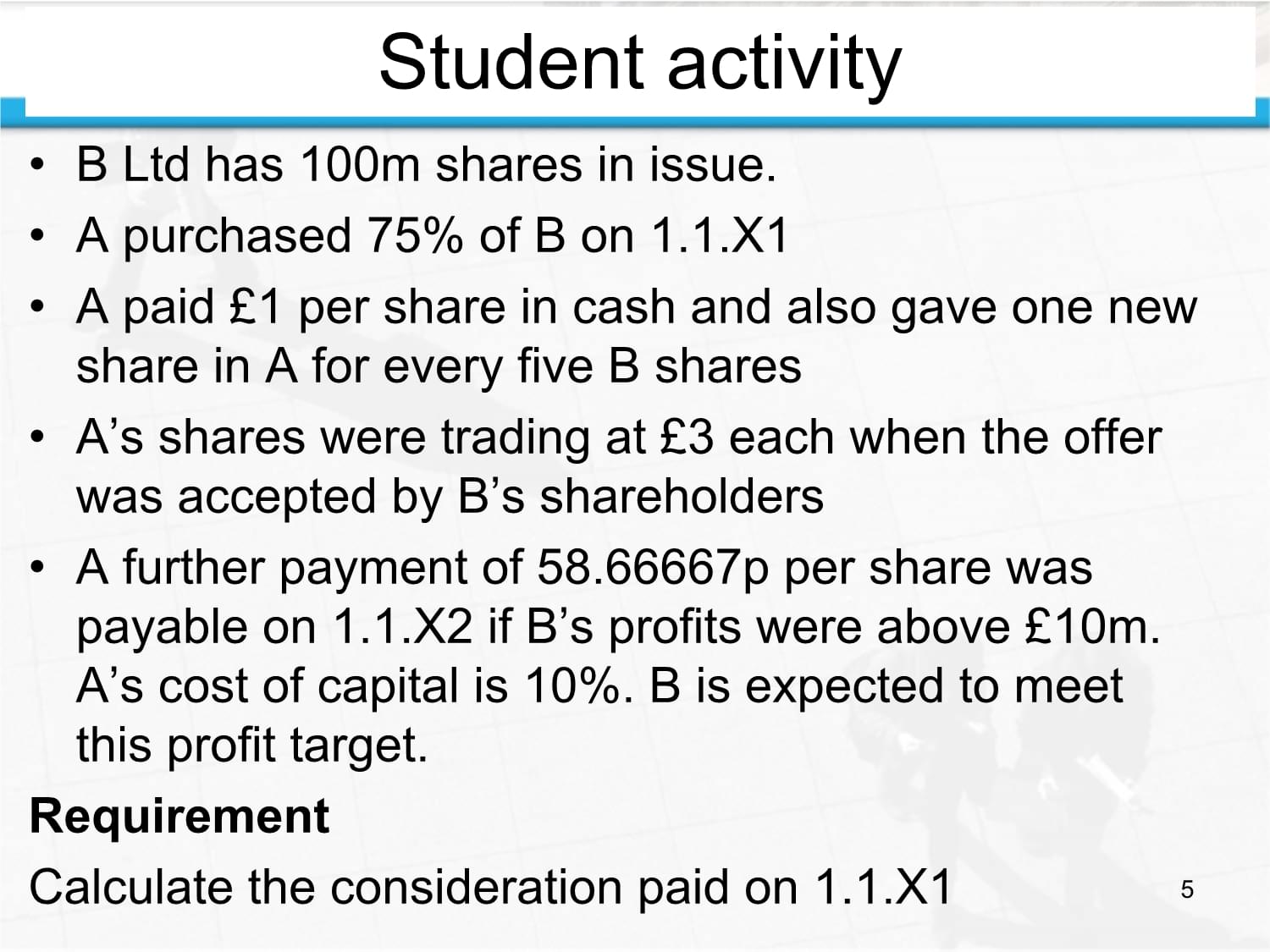

4、erred consideration is added to the purchase price. Over time, the unwinding of the discount is added to finance costs (not goodwill!)4Student activityB Ltd has 100m shares in issue.A purchased 75% of B on 1.1.X1A paid 1 per share in cash and also gave one new share in A for every five B sharesAs sh

5、ares were trading at 3 each when the offer was accepted by Bs shareholdersA further payment of 58.66667p per share was payable on 1.1.X2 if Bs profits were above 10m. As cost of capital is 10%. B is expected to meet this profit target.RequirementCalculate the consideration paid on 1.1.X15AnswerCash

6、of 75m was paid (100m*75%*1)A purchased 75m shares in B 15m new A shares were issued (one for five), worth 15m*3=45m75m*0.5866667=44m will be paid - 40m at present value (44m/1.1=40m)Total consideration is 75m+45m+40m=160mNB only 75m will be shown in the consolidated statement of cash flowsNB there

7、will be a 4m finance charge (40m10%) in 20X1. 6The treatment of differences at acquisition date “fair value accounting”The identifiable assets and liabilities of the subsidiary are valued at fair value.The adjustments to assets and liabilities at acquisition date are recognised on the consolidated s

8、tatement of financial position with a corresponding entry to purchased goodwill.Increasing fair values of assets will decrease purchased goodwill.7Measuring the Net Assets AcquiredHow to recognise and measure assets and liabilities that exist at the acquisition date:Assets other than intangibles if

9、probable that associated future economic benefits will flow to the acquirer, and fair value can be measured reliably, value at fair value.Intangible assets if separable from goodwill and fair value can be measured reliably, value at fair value.Liabilities other than contingent liabilities if there i

10、s a probable outflow of economic benefits, and fair value can be measured reliably, value at fair value (relief value). No recognition of future losses or restructuring costs unless previously recognised by the acquiree.Contingent liabilities if fair value can be measured reliably then the contingen

11、t liability needs to be included (even if only possible and not recognised under IAS37).PURCHASED INTANGIBLESIntangibles acquired in a business combination must be recognised separately from goodwill if: Separable or arise from contractual or other legal rights; andFair value can be reliably measure

12、d.Normal test for probability of future economic benefits deemed to be satisfied for acquired intangiblesThis is a weaker rule than the normal test for recognition of separate intangibles under IAS38 which requires an active marketExampleRyan Giggs has played over 1,000 games for Manchester United.H

13、e has been with the club for over twenty years.He could be sold to another club today and the club that purchased him could recognise the transfer fee as an intangible non-current asset. There is an historical cost that can be capitalised and amortised.Before Manchester United were taken over Giggs

14、value could not be recognised under IAS38 as there is no readily ascertainable market value (fans chant theres only one Ryan Giggs and there are no identical Ryan Giggs being traded daily).However, in 2005 Manchester United were taken over by the Glazer familys company red football limited for 1.2bn

15、. Under IFRS3 Giggs value could have been included as a separable intangible in Red Footballs consolidated accounts (however, all I can see on FAME is 557m of intangible assets). Recognising the value of players would have reduced the purchased goodwill figure.Examples of IntangiblesMarket-related i

16、ntangiblesTrade marks, trade names, internet domain names, trade dress, mastheads etcCustomer-related intangiblesCustomer lists客户名单, order backlog未完成订单, customer contracts etcArtistic-related intangiblesPlays, operas, ballets, books, magazine, musical works, pictures, photos, videos etcContract-base

17、d intangiblesLicensing & royalty agreements, lease agreements, franchise agreements etcTechnology-based intangiblesPatented & un-patented technology, computer software, databases, trade secretsFAIR VALUESAssetMeasureReceivablesPresent value (unless short-term)Finished goodsSelling price less selling

18、 costs less reasonable profit allowanceWIPRaw materialsAs finished goods above, less costs to completeReplacement costProperty, plant etcMarket value (or FV less costs to sell for assets held for resale under IFRS 5)Intangible assetsRefer to active market if possible, if not, estimate using all avai

19、lable informationFAIR VALUESLiabilityMeasurePension fund deficitActual deficitTax liabilitiesAmount receivable or payable assessed from perspective of combined entityAdditional deferred taxBased on fair value of acquired entitys assets compared to tax basesPayables/ onerous contractsPresent value (u

20、nless short-term) of amounts to be paidContingent liabilitiesAmount a third party would charge to assume the contingent liability use market value, not a minimum, maximum or most likely cash flowFAIR VALUESCorrection of provisional fair valuesIf done within 12 months of acquisitionRestate assets, de

21、preciation, goodwill retrospectively from acquisition dateAdjust comparativesAfter 12 months, only restate retrospectively for errors see IAS 8 Accounting policies, changes in accounting estimates and errorsPre-acquisition and Post-Acquisition reserves Up to now we have only been preparing consolida

22、ted SOFP on the acquisition dateWe now have to consolidate in the years following acquisition.Rules:Pre-acquisition reserves are frozen into the goodwill calculation.Parents share of post-acquisition reserves are included in consolidated group reserves.15Pre-acquisition retained earningsAny profits

23、or losses of a subsidiary made BEFORE the date of acquisition are referred to as pre-acquisition retained earnings.There may also be revaluation reserves, share premium and other relevant reserves represented under the equity of the subsidiary at the date of acquisition. These are represented by the

24、 equity of the subsidiary that existed at the date of acquisition.They have all been generated BEFORE the date of acquisition.16Post-acquisition retained earningsAny profits or losses of a subsidiary made AFTER the date of acquisition are referred to as post-acquisition retained earnings in the cons

25、olidated financial statements.These are included in the equity of the subsidiary existing on the date when we are preparing the consolidated SFP.17ExampleAssume that Company A acquired 80% of the ordinary shares in B for 175,000. At acquition date on 1.1.20X1, B had the following equity elements:Sha

26、re capital 1 each : 100,000Share premium : 30,000Retained earnings : 60,00018ExampleStatements of financial position for A and B as follows:Financial positionA BAt 31.12.20X1(000)(000)Investment in B175-Other assets625400TOTAL ASSETS800400Ordinary shares 1 each 200 100Share premium 50 30Retained ear

27、nings 175 110Equity425240Liabilities375160TOTAL EQUITY & LIAB.80040019(000)Parents portion (80%) at acquisitionParents portion (80%) at post-acquisitionNon-controlling interest (20%)Ordinary shares10080-20Share premium 3024-6Pre-acq. RE 6048-12Post-acq. RE 50-4010TOTAL1524048Cost of investment175Pur

28、chased Goodwill 23 Why there isnt NCIs share of goodwillEquity analysis203820% of 240Consolidated SOFPConsolidated Financial Position AAt 31.12.20X1(000)Goodwill23(as above)Other assets1,025(625+400)TOTAL ASSETS1,048Ordinary shares 200Share premium 50Retained earnings 215 (175+40)Equity465Non-contro

29、lling interest48(as above)Liabilities535(375+160)TOTAL EQUITY & LIAB.1,04821Consolidated statement of comprehensive eWhere a parent has subsidiaries, joint ventures or associates a consolidated e statement is required. By including subsidiaries the aim is to show the results of the group for an acco

30、unting period as if it were a single entity.The revenues and expenses of a subsidiary are included in the consolidated financial statements FROM the acquisition date. The revenues and expenses of a subsidiary are included in the consolidated financial statements UNTIL the date on which the parent ce

31、ases to control the subsidiary.221.1.20X1 -31.12.20X1AB(000)(000)Revenue250120Cost of sales(120)(40)Gross profit13080Operating expenses(35)(15)Profit before tax9565Tax expense(20)(15)Profit for the period7550ExampleReferred to in the previous example, the summarised statements of comprehensive e for

32、 the year ended 31.12.20X1 were as follows:23(000)Revenue370(250+120)Cost of sales(160)(120+40)Gross profit210Operating expenses(50)(35+15)Profit before tax160Tax expense(35)(20+15)Profit for the period125Profits can be attributed to:Owners of the parent115Non-controlling interest10( 50 x 20%)125Con

33、solidated Statement of Comprehensive e for year to 31.12.X124Post-acqn profit31.12.20X1000(+) Opening balance of group retained earnings Company A (175-75) Company B: (60-60)x80% 100(+) Group profit115(-) Dividend paid by the parent-(=) Closing balance of group retained earnings215Changes in group r

34、etained earningsChanges in group retained earnings can be followed by a statement based on the previous example as below:25SFPSCIIntra-group transactions: unrealised profits in inventoriesAny intra-group trading needs to be removed to avoid overinflating revenues. For example, two companies in the s

35、ame group could buy and sell between them to boost the top line. So sales of one group company cancel with purchases of the another. If there is profit still in inventory because intra-group sales have not been sold to an outside party, then the reduction in inventory value is deducted from group co

36、st of sales. Otherwise inventories will be artificially overstated in value.Intra-group sales may have resulted from “up-stream” or “down-stream” transactions.26Up-stream / down-stream27SubsidiaryParentUp-streamSubsidiaryParentDown-streamCr InventoryDr Cost of sales of subsidiary (reduces value of N

37、CI)With profit in inventoryCr InventoryDr Cost of sales parentWith profit in inventoryStudent Activity28(Use A and B form the previous examples)During 20X1 A sold 90,000 of goods to B. A used a mark-up of 50%. B still has 30% of these goods in inventory at the year-end.During 20X1 B sold 20,000 of g

38、oods to A. B has a profit margin of 50%. At the year-end A still had 60% of these goods in inventory.RequiredShow how you would cancel out these group transactionsAnswer29Sale to BThe 50% mark-up gives 30,000 of profit on sale. 30% is still in stock therefore profit in inventory is 9,000 (30% of 30,

39、000).Reduce group sales by 90,000 and reduce group purchases by 90,000Increase group cost of sales by 9,000 and reduce group inventory by 9,000Sale to AThe profit margin of 50% gives a cost of 10,000 and a profit of 10,000. 60% is still around so profit in inventory is 6,000.Reduce group sales by 20

40、,000 and reduce group purchases by 20,000Increase group cost of sales by 6,000 and reduce group inventory by 6,000. Move 1,200 of loss from parent to NCI(000)Revenue260(250+120-90-20)Cost of sales(65)(120+40-90-20+9+6)Gross profit195Operating expenses(50)(35+15)Profit before tax145Tax expense(35)(20

41、+15)Profit for the period110Owners of the parent101.2Non-controlling interest8.8( 44 x 20%)110Consolidated Statement of Comprehensive e for year to 31.12.X130Post-acqn profit (B has profit of 50-6=44 )Consolidated SOFP as at 31.12.X1(000)Goodwill23(as above)Other assets1,010(625+400-9-6)TOTAL ASSETS

42、1,033Ordinary shares 200Share premium 50Retained earnings 201.2 (100+101.2)Equity451.2Non-controlling interest46.8(240-6)*20%) (or 38+8.8)Liabilities535 (375+160)TOTAL EQUITY & LIAB.1,03331Other adjustmentsAdditional depreciation charges over the increase in fair value of depreciable assets since aqui

温馨提示

- 1. 本站所有资源如无特殊说明,都需要本地电脑安装OFFICE2007和PDF阅读器。图纸软件为CAD,CAXA,PROE,UG,SolidWorks等.压缩文件请下载最新的WinRAR软件解压。

- 2. 本站的文档不包含任何第三方提供的附件图纸等,如果需要附件,请联系上传者。文件的所有权益归上传用户所有。

- 3. 本站RAR压缩包中若带图纸,网页内容里面会有图纸预览,若没有图纸预览就没有图纸。

- 4. 未经权益所有人同意不得将文件中的内容挪作商业或盈利用途。

- 5. 人人文库网仅提供信息存储空间,仅对用户上传内容的表现方式做保护处理,对用户上传分享的文档内容本身不做任何修改或编辑,并不能对任何下载内容负责。

- 6. 下载文件中如有侵权或不适当内容,请与我们联系,我们立即纠正。

- 7. 本站不保证下载资源的准确性、安全性和完整性, 同时也不承担用户因使用这些下载资源对自己和他人造成任何形式的伤害或损失。

最新文档

- 2026年福建省南平市单招职业技能考试题库(典型题)附答案详解

- 2026届河南省普通高中毕业班高考适应性测试理科数学试题

- 2026年漳州工勤人员考试试题及答案

- 扎囊县2026届四年级数学下学期期中调研模拟试题(含答案)

- 2026学年河南省沁阳市五年级数学期末高分预测盲点排查题(附答案)详细答案和解析

- GB/T 3810.2-2026陶瓷砖试验方法第2部分:尺寸和表面质量的检验

- 2026年全国中级注册安全工程师之安全生产法及相关法律知识考试历年考试题详细参考解析

- 2026学年湖南省常宁市五年级语文期末自测高频题(详细参考解析)详细答案和解析

- 2026陕西铜川市宜君县大学生到政府机关见习20人考试模拟试题及答案详解

- 2026年南昌市东湖区住房和城乡建设局人员招聘笔试参考试题及答案详解

- GB/T 24026-2026环境标志和声明足迹信息交流的原则、要求和指南

- 2026菲律宾椰子行业市场现状供需分析及投资评估规划分析研究报告

- IT系统日常运维管理SOP文件

- T∕TAF 293-2025 物联网蜂窝模组与电信智能卡兼容性技术要求和测试方法

- 2026年全国硕士研究生招生考试政治试题及其答案

- 2026年国家职业卫生考试试题及答案

- 工程造价审计审计重点及难点分析

- 永辉超市门店SOP标准作业流程制度规定

- 国开期末考试《行政领导学》机考试题及答案

- 呼吸科绩效考核制度

- 2025年贵州黔东南凯里市事业单位第二轮公开招聘工作人员(医疗岗28名)笔试历年典型考题及考点剖析附带答案详解试卷2套

评论

0/150

提交评论